Combining Active and Passive Strategies with customisation

There’s more to the question of whether to invest passively or actively than that high level picture, however. Active strategies have tended to benefit investors more in certain investing climates, and passive strategies have tended to outperform in others. For example, when the market is volatile or the economy is weakening, active managers may outperform more often than when it is not. Conversely, when specific securities within the market are moving in unison or equity valuations are more uniform, passive strategies may be the better way to go. Depending on the opportunity in different sectors of the capital markets, investors may be able to benefit from mixing both passive and active strategies — the best of both worlds, if you will — in a way that leverages these insights. Market conditions change all the time, however, so it often takes an informed eye to decide when and how much to skew toward passive as opposed to active investments.

If pursuing a “best of both worlds” approach, it is also worth noting that achieving consistently successful active management has historically proven more difficult within select asset classes and portions of the market, such as among the stocks of large U.S. companies. As a result, it may make sense, if appropriate for your situation, to veer a bit more passive in those areas and rely more on active investing in asset classes and parts of the market where it has historically proven more profitable to do so, such as among international stocks in the emerging markets and those of smaller U.S. companies.

Some investors have very strong opinions about this topic and may not be persuaded by our nuanced view that both approaches may have a place in investors’ portfolios. If your top priority as an investor is to reduce your fees and trading costs, period, an all-passive portfolio might make sense for you. In our experience, investors tend to care more about factors like risk, return and liquidity than they do fees, so we believe that a mixed approach may be beneficial for all investors — conservative and aggressive alike.

As with many choices investors face, it really comes down to your personal priorities, timelines and goals.

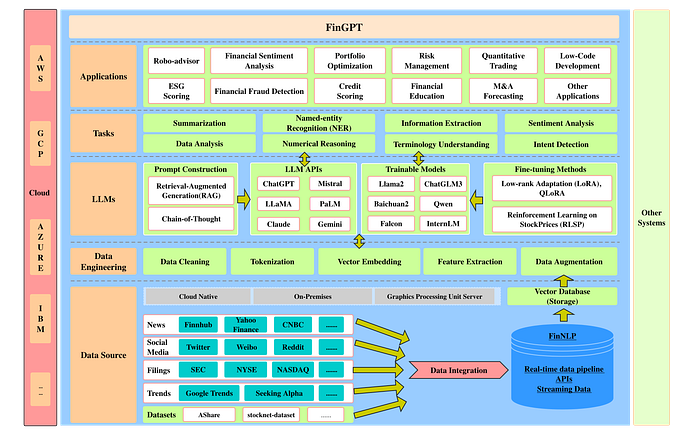

Upside’s vision of a possible future.

Traditional Actuarial Investing models would have it that at the outset of our careers, where we demonstrate the lowest income, but greatest time, we should take the greatest risk.

We believe this model to be over simplistic and causally flawed in the sense that losses are felt in real world terms at the outset of ones career, whereas they maybe more objectively observed as percentages in later life.

We also note that this approach pays little or no attention to the economic situation at the outset (young family, university fees etc) or indeed the negative long term feedback loop that may be achieved through an early (negative) experience.

We therefore believe in a more tailored approach, whereby a saver or investor may more dynamically adjust risk based upon the prevailing conditions, in much the same way as a car would drive more quickly on a straight, dry and well lit road, but slow at night in the rain or around corners.

The specifics would then come down to the car, the driver and the destination.

We envisage a merger of savings and investment where the principles of putting money aside on a week by week or month by month basis remains. Yet instead of having this money statically sat in either a deposit or locked up in a term or investment account, this money is moved dynamically into an investment portfolio which affords the same liquidity as a fiat/ cash account would.

Similarly, we envisage this portfolio as comprising variable weight layers, containing a foundational (yield focused low risk hyper diversified) element, an expressive passively (Bundles) — active layer and a true active active layer.

The interplay between the layers being the primary expression of risk. Creating a portfolio of some 200 investments with a weighting range per company from 0.3% to 10% based upon the users specific desires and confidence (Secondary Risk).

The key point here being that the user can select tightly managed, thematic bundles of actively managed (but passively selected) companies that allow for a hyper personalised expression of views, with an element of single stock and foundational layer comprising the aggregate risk.

This dynamic, and guided approach to both Primary and Secondary Risks, allows every user to build their own personalised portfolio, but with guidance and comprising a dynamic amount of active and passive investments, which may vary over time based upon the prevailing macro, market and personal economic conditions.

Why has this not been done?

The overarching challenge has been one of scale. How to scale the product for cost, for complexity and construction.

- Cost — only in the last 5–10 years has the cost of execution, settlement and onboarding moved in such a way as to allow single account setup (as demonstrated by the rise of the trading app)

- Complexity — Constructing Portfolios of Investments has historically been sat behind walls/advisors and pre-packaged products to make consumption more straightforward, however with the rise of financial literacy and engagement this is now changing

- Construction — Until now the challenge for Roboadvisors is the financial model, with the product created externally, little of the revenue is able to be retained given the payaway. In addition given the nature of the ETF and Index products the look through is almost impossible to achieve dynamically.

These problems do not exist in Private or Investment Banks which is why these products (hyper personalised) are afforded to hedge fund investors, however the model is highly expensive and non-scalable.

By solving the scalability issue it is possible to drive costs down dramatically, reshaping the way users may access products and services.

Solving the scalability problem

To illustrate how Upside has approached this challenge of scale, we will focus on the Bundle layer as the most complex.

The institutional world shows us that actively managed portfolios, while offering the possibility of both generating alpha and protecting against losses in market downturns, come with the scale limitations and costs driven by the specialised portfolio management teams.

The challenge is therefore how to create unlimited product(s) with a passive fee increment.

Upside has sought to address this by creating dynamic alpha products that are autonomously created by leveraging three core pillars:

- Quantitative and Artificial Intelligence Based Stock Screening Models.

- Wisdom of the crowd.

- Superforecasting.

By combining these inputs Upside can derive a series of ‘scores’ for each company in the specified universe, along with its various inclusion parameters. Implying that for any given thematic Bundle, there is a defined and ranked universe of eligible names which are constantly optimised for their portfolio benefits as well as their idiosyncratic properties.

This allows for a theoretically unlimited number of low cost high alpha products that can be overseen by a fixed number of people allowing for enormous economies of scale and a persistent downward pressure on unit costs.

When these Bundles are combined with a user-determined layered weighting ratio, and single stock selections the possible combinations of portfolios become similar to the play lists of Spotify users!